Past year was a good one for me in terms of learning. And i want to share some key ideas I inculcated in my framework for investing, and would love to have readers feedback.

-Thinking about the E in P/E. Many times we err to take the current steady state earnings of the company for granted and attach a multiple to it. We should think rigorously about how robust/sticky are current revenues and earnings, before thinking about growth.

E.g When RS software started plummeting, i was hearing from lot of market participants that its getting cheap on FCF yield, p/e etc. Now we are seeing that the company’s revenues and profits have started declining, hence it was a futile exercise to attach multiples to previous year’s earnings.

-At times we get carried away by the fancy of investing in turnaround stories/high growth sunrise sectors. My sense is we should wait for some kind of visibility to show in quantitative data, meaning, sales and profit figures.

-Learning deeply about one particular subject/ industry. Your mental strength will be tested during times of market turmoil, and it serves good to have a good sense of business value and focussing on it.

“A certain amount of immersion in a topic will provide disproportionately more insight than an executive summary.” Silver, Nate

-Some “first principles thinking,” a mode of inquiry that relentlessly pursues the foundations of a problem …

Collating key facts independently..First forming a hypothesis and then using qualitative and quantitative data to support/deny it.

e.g Is the demand secular/cyclical, runway for growth, disruption threat etc

-Markets are rapidly expanding in many sectors we are seeing domestically e.g Dairy, Jewellery, Advertising, Pharmaceuticals etc but the consolidation has to happen sooner or later, or already happening in some micro markets, see how good is your company’s resilience to competition.

-Missing forest for the trees …Its good to go deep into a subject but don’t fall into the familiarity trap that if you know too many details about the company, your thesis is strong …Don’t lose sight of the key questions.

-Keeping the idea pipeline rich, where you may not invest but keep a track of certain business and key factors to jump in at the opportune moment. Or a you may feel like a exiting a holding when certain factors go wrong and having your next best idea ready comes in handy.

-Liquidity in portfolio is good , it gives you an option value for opportune times in the market.

-Paranoia is good … Keep visiting your key points in the thesis again periodically as most of the times understanding of a company increases with time for which you have been invested.

P.S. Interaction with lot of fellow investors have helped me shape my thinking on above mentioned areas and i am deeply thankful to them for sharing their wisdom in a more than generous manner.

India Real Estate market

In the first post, I talked about Real estate market in general. Here, I want to examine the realities in India Context.

Few peculiarities about India :

In the past, Black money has supported price levels; and fair price discovery in the market has always been hindered as real estate was the best place to store large sums of black money.

Also, the conventional wisdom of real estate being the safest investment, led to huge amount of household savings being funneled here.

But, now since past few years it has been getting difficult to invest in real estate with black money, as circle rates have been rising throughout the country. Also, a loophole where stamp duty was paid on circle rates but transaction was done way below this value has been plugged, with any transaction done below circle rates attracting penalties for both buyer and seller.

And, with the advent of new central government in 2014, there have been indications of massive policy changes in this sector.

Some salient features are:

With proper implementation, this will bring transparency, better access of capital, consumer confidence for the sector.

The flip side is with curbing of black money, real estate may no longer be an attractive investment for majority, leading to price levels which may be significantly lower than current ones. Currently it is difficult to predict how will the scenario play out.

India as an investment case

India has the uniqueness of unmet and increasing housing demand and simultaneously huge unsold inventory; one needs to delve deeper into price segmentation of demand to ascertain reasons for this.

Affordable housing: It refers to housing for economically weaker sections (EWS) and lower income groups (LIG) where income ranges from 100000-200000 INR per annum. The majority of housing shortage 80-85% is concentrated here; and also has the highest demand-supply mismatch.

Government is trying to provide a policy push here, easing the land acquisition for affordable housing projects by introducing amendments in the Land acquisition bill.

Previously, this section lacked access to housing finance due to lack of income proofs, nil past experience of banking etc. Now, we have housing finance companies specializing in providing finance to EWS/LIG sections of society. They have developed their strength by a better understanding of income patterns, cash flow patterns of this group and hence tailoring a suitable loan product.

Also, the interest of developers in this previously ignored space is rising with lot of pilot projects being undertaken and some companies completely concentrating on affordable housing space. But, these projects are tricky in nature with very little room for time and cost overruns and lower margins.

Middle Income Housing: It refers to housing for middle income group where annual income ranges from 300000-1000000 INR. This market accounts for round 7-8% of housing demand

The incremental demand should be strong with increasing urbanization and mid-income households expected to triple from current 30 million to 110 million by 2026.

At the national level, the government estimated the total urban housing shortage at 18.78 million units in the 12th five-year plan . Of this, about 2.47 million units would arise from the top eight cities (Ahmedabad, Bengaluru, Chennai, Delhi-NCR, Hyderabad, Kolkata, Mumbai, and Pune) in India, with LIG (0.85 mn units) and MIG (0.88 mn units) segments likely to account for the major chunk (about 80%) of the total demand.

Luxury housing: As the name suggests, it is meant for people with income upwards of INR 12-15 lakhs per annum. These houses are typically greater than 1200 square feet in size and no ceiling on the higher side.

In India HNI population has shown huge growth in past few years with 2012, clocking an impressive 22% growth and is expected to continue growing by 10-12% each year for next five years.

This space provides fat margins to developers but they have to keep coming with new innovative offerings (branded residences, golf townships etc) providing luxury living.

A good capital allocator

A good capital allocator in this sector tends to plan ahead for at least a 5-7 year cycle with prudent demand estimation, project planning, attracting low cost capital and having a solid risk management framework in place(see previous post).

There is inherent cyclicality in real estate as discussed in previous post, he may take advantage of peak and troughs; recessionary times can be used for adding land parcels at opportunistic valuations( since A real estate downturn may not necessarily coincide with downturn in capital markets)

Present situation with developers

Currently, majority developers are mired in debt, have huge piles of unsold inventory, not meeting cost of debt with refinancing looming due to their overconfidence in the previous boom times, where they forgot the discipline needed.

If the government is successfully able to implement its planned measures for real estate sector, increase transparency, bring back consumer confidence, and with important support from reversing of the interest rate cycle, a lot of wealth will be created during the next upswing, but one has to choose the pockets carefully.

I am not investing as of now but will be watching keenly from the sidelines.

There has been general buoyancy of valuations in the market. So, the quest for value often takes us to neglected corners of the market. One such place for me has been Real estate sector; so I set about understanding the dynamics here.

Throughout the global history, Real estate has shown remarkable consistency in exhibiting cyclical patterns. One primary reason for this has been the time lag between demand and supply(It takes long time to add new inventory to real estate market once when its needed, and then developers not giving weightage to cyclicality tend to keep erecting buildings till there is a widespread recession).

Other significant driver for this cyclicality is Interest rates and credit supply.

One of the early works to demonstrate the characteristics and phases of real estate cycle were published by Henry George in late 19th century. His findings were as follows :

Phase I RECOVERY ….. Land prices are at depressed lows, Unmet demand for residence and business needs is increasing. Interest rate cycle has already peaked and maybe trending downwards.

Phase II EXPANSION…. Occupancy begins to exceed the long term average ,Increase in rental growth and real estate prices, Pace for new development increases.

Speculators then jump in to profits from change in prices, also there is surge in volume of credit, written on land being collateralized at higher values.

Investors believing current rates justifying future growth keep on buying at inflated prices and developing new projects.

Phase III HYPERSUPPLY… Abundance of supply in the market, Early signs of trend reversal with rise in unsold inventory,rent growth rates drop lower and lower. Huge expansion of credit in previous phases may lead to increase in interest rates consequently higher mortgage payments.

Phase IV RECESSION… Rate of growth of unsold inventory accelerates, rising interest rates, lower profits for developers on account of lower rents than anticipated and high unsold inventory.

Homer Hoyt, a leading land economist of 20th century believed a typical real estate cycle to be around 18 years using data of land prices and volume of transactions in many cities of USA. But, In India, Asia, Middle East etc empirical evidence from past 3-4 decades suggests cycles have been shorter and in the range of 8-10 years.

Owing to this inherent cyclicality, it is imperative for a real estate player to act with prudence and keep track of certain factors that affect demand and supply. This in turn will help them to calibrate their strategy and resource allocation.

A.Demographic factors…shape demand because of population growth, migration, household size, age distribution and change in family structure

B.Economic factors… household purchasing power, interest rates, foreign investments etc

C.Regulatory factors… have an impact on providing transparency and increasing confidence of the buyers

D.Political factors… such as an unstable region may cause buyers to shun investments and look for liquid instruments. (Think Regions of Telangana, especially Secunderabad/Hyderabad)

To survive a market downturn a developer should have robust risk-management framework in place. This business has volatile revenue streams and its necessary to balance the portfolio with certain recurrent revenue streams(leased assets) to meet cash needs during recessionary times. Also, a level of risk be defined with which stakeholders are comfortable and consequently a debt/equity limit be set. And, too often during expansionary phase, it’s seen, developers start taking all kinds of projects across value chain/segments perceiving low risks and future profits and wander away from core expertise(Think Shopping malls during last real estate boom in india ,Also this month’s cover story in Business Outlook). The management’s aim shouldn’t be to profit the most during Boom times but to create sustainable value for stakeholders.

In 1986, Warren Buffett detailed his valuation method. He stated that the value of a company is simply the total of the net cash flows (owner earnings) expected to occur over the life of the business, discounted by an appropriate interest rate. He defined owner earnings as follows:

The objective of this post is to discuss the conundrum of valuing a company when there is a significant difference between reported accounting profits and Owner’s earnings . The first company is Dish TV. I first remember coming across the Cable TV business model reading this excellent biography of John Malone, For 20-25 years, which Malone served as TCI( Tele-communications Inc, a Cable giant in US), company hardly reported any accounting profits, taking advantage of allowed accelerated depreciation under US tax laws, but inarguably was a huge wealth creator (From his debut in 1973 until 1998 when the company was sold to AT& T, the compound return to TCI’s shareholders was a phenomenal 30.3 percent, compared with 20.4 percent for other publicly traded cable companies and 14.3 percent for the S& P 500 over the same period.A dollar invested with TCI at the beginning of the Malone era was worth over $ 900 by mid-1998).

One primary reason was the strong cash flows of the company which Malone used brilliantly to acquire assets all around the country and gain leadership position. In a recent discussion, i had with a fellow investor on twitter , we talked about similar strategy adopted by DTH players in India , frontload depreciation and no taxes. Dish TV hardly posts any accounting profits but has already started generating FCF from last year. And, analysts expect it to post FCF of ~100 crs this fiscal year.

The second company is Tata communications This company is in a turnaround phase and most likely will report accounting profits in future, but a closer look at robust cashflow numbers and management guidance about mantainence capex will tell you that this company already on a steady path.

Finally, i would like to add AMAZON, ( the retail giant we all know about ) Amazon’s management has always stated their goal is to maximize free cash flow per share , and even after having negligible profits for past few years , it has been able to grow relentlessly. Although, Amazon differs from former two examples on two fronts,lack of operating profits and a float(owing to its negative cash conversion cycle) .

Yes the market pays for multiples of accounting profits but may be, one of the ways to make good returns is buying before the story gets apparent in the numbers. Its easy to figure out the conventional wisdom on surface from the numbers, but its always better to delve deeper and weigh the underlying qualitative aspects.

The Value of this book comes in situations where stakes are sufficiently high and natural decision-making process can lead to a suboptimal choice.

1.The outsiders view

– Three factors determine the outcome of your decision

a. how you think about the problem b. subsequent actions c. luck

-Incorporating outside view into your decision

a. select a reference class

b. Asess the distribution of outcomes…..a 80% probability of 50 % gain and 20% probability of 70% loss is not healthy although positive expected value

c. Make a prediction

d.assess the reliability of your prediction and fine tune.

2. Open to options

-When stakes are sufficiently high, we must slow down and swing light over the range of all possible outcomes.

-Stress is often very helpful. The classic response is energy mobilized to your muscles by increasing your heart rate, blood pressure and breathing. It also aids your sensory system.

– Stress is bad , if its constant.

Psychological stress creates a sense of urgency that inhibits consideration of options with distant payoffs, compelling poor decision-making.

-Avoiding tunnel vision

3.The expert squeeze

-In a domain with probabilistic( not rule based) , wide range of outcomes , experts perform worse than collectives.

– The diversity prediction theorem tell us that diverse crowd will always predict more accurately than average person in the crowd

three conditions must be in place for this theorem,

a.Diversity

b. aggregation . it ensures that market consider’s evryones information.

c. incentives. It helps reducing individual errors by encouraging people to take part only when they think they have an insight.

When one or more of the three wisdom of crowd conditions are violated, the collective error can swell.

Some suggestions to make the expert squeeze work in your favor.

…..algorithms, regression, simulations etc

-Peer pressure

–fundamental attribution error…tendency to explain behavior based on individual’s understanding versus the situation….(situation is generally more powerful than people)

-Priming…..the incidental activation of knowledge structures by the current situational context

-Status Quo bias.. one should ask this question (If we did not do this already, would we, knowing what we know now, go into it.

Tools to improve awareness:

a.Being aware of your situation.. focusing on process, keeping stress to an acceptable level, being a thoughtful choice architect, making sure to diffuse forces that encourage negative behaviors

And, coping with subconscious influences

b.Consider the situation first and the individual second.

c.Watchout for the institutional imperative…avoiding peer pressure

d.Avoid inertia

5.More is Different

Complex adaptive systems- the whole is smarter than its parts

Complex systems have three parts

Constellation matters more than its brightest star…

Dealing with a complex adaptive system

a.Consider the system at correct level…..e.g. seeing stock market at market level rather than at participant level.

b.Watch for tightly coupled systems.. when agents lose diversity and behave in a coordinated fashion, a complex adaptive system can behave in a tightly coupled fashion

c.Use simulations to create virtual world

6.Evidence of circumstances

-Embracing a strategy without fully understanding the conditions under which it succeeds or fails

Difference between correlation and causality….

Three conditions must hold to make a claim that X causes Y.

1. X must occur before Y

2. Second is a functional relationship between X & Y

3.The final condition is that for X to cause Y, there can’t be a Z that causes both X and Y

Correctly considering circumstances in decision making:

a.Ask whether the theory behind your decision making accounts for circumstances… b.Watch for correlation and causality trap,

c.Balance simple rules with changing conditions…revisiting your investment thesis when drivers are changing

d.There is no best practice in domains with multiple dimensions.

6.Grand-ah-whooms

Feedback can be negative or positive , and many systems contain a healthy balance of two ..Too much of either type of feedback can leave a system out of balance..

Positive feedback…fads and fashion

Negative feedback….Arbitrage

Small incremental changes can lead to large scale effects..

Power law…Few of the outcomes are really large and most observations are small.

The problem of induction and reductive bias…we’re better off focusing on falsification than on verification.

Social influence can be the engine for positive feedback.

Coping with systems that have phase transitions.

7.Sorting Luck from skill

–System combining luck and skill will revert to mean over time.

-Thinking you’re special is first and basic mistake.

-Halo effect..judging based on appearances, impressions..

Avoiding mistakes associated with reversion to mean:

CONCLUSION

Consider 2nd and 3rd order consequences.

Incentives

Leaders must develop empathy. If you’re the decision maker and others live with the consequences of your choices, understanding their perspectives and feelings is key to effectiveness.

Get feedback.

Decision making journal—how you came to that decision and what you expect to happen

Checklist…General enough to allow for varying conditions yet specific enough to guide action

Perform a pre-mortem

Knowing that there will be Unknowns (known unknowns and unknown unknowns)

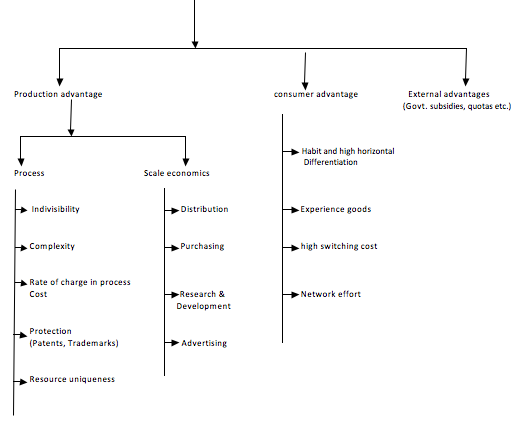

A very simplistic framework to think about the kind of Strategic advantages a firm can have. This has been taken from an excellent paper titled Measuring the moat written by Michael Mauboussin and i have rearranged it in a tabular format.

Firm specific

Value created = Willingness of buyer to pay – opportunity cost of supplier

“Simplicity is the ultimate sophistication” – Leonardo Da Vinci

KRBL, is India’s leading exporter of branded basmati rice and owner of the largest rice milling capacities, has consistently outperformed peers in past few years. A strong brand and an efficient wcap mgmt have enabled KRBL to tap growth in Basmati rice industry.

Domestically also, the demand for basmati rice has been growing at healthy rates ,12-15% CAGR for past ten years and the trend is expected to continue with increasing disposable income .

BUSINESS

Both the basmati and non-basmati sectors present the organised players with tremendous opportunities since organised players have a low presence in both the segments. The former is a high margin export oriented segment while the latter provides the alternative of value-added products derived while processing. The fragmented players lack the technology and expertise in procurement process required for these high end activities. Hence, the large players have the scope to take up the advantage and capture the market.

There are more than 139,000 rice processing mills in India processing about 132 mn tonnes of paddy. Out of this, a little over 25% (35,000) are classified as modernised rice mills.

Effective procurement: Quality is the most important characteristic for maintaining brand recognition in the market. This requires effective procurement process for paddy. Large players can procure the bulk volume through upfront payments to farmers and middlemen

-product/ service Usage (essential or lifestyle)

Lifestyle product , better taste , prices vary widely depending on brands , starting form Rs 80-90/kg

-Product/Service type (brand or commodity )

The market for basmati rice is moving towards a more organised one with consumer preference increasing towards branded choices

–In last two years in India , production of paddy(basmati variety) has not shown growth pushing up prices by north of 20% and yet the demand has been solid.

Understanding the supply

-Export of Basmati in 2013 4.02 Mn tonnes ( volume )

4.5 Bn USD ( value)

– Company has 30% share in the organized domestic market and 25% share in the branded basmati rice exports market

Raw Material

Paddy is the main raw material for the company and is the main component of costs for the company(`80% of sales)

The prices of paddy vary season to season based on production which is a function of weather, area under cultivation , plantation techniques, hybrid varieties etc

Industry Structure and competitors

Basmati exports industry has 5-6 big players enjoying majority of the sales. And, major competitors are KRBL, REI agro, Kohinoor, LT overseas

COMPETITIVE ANALYSIS/moating points

The company enjoys a huge scale advantage in terms of procurement, distribution, advertising and R&D.

KRBL ties up directly with the farmers for procurement of paddy, providing them technical expertise leading to better yields , reduction in risk by providing good value without involving intermediaries .

Contract farming forms 80% of the raw material purchase of the company. And ensures timely availability and quality of grains for the company .

The company has 2,40,000 acres under contract farming.

Pan-India distribution network with presence at 6,40,000 retail outlets across 28 states

KRBL has highest milling capacity of 195 MT/hr which is significantly ahead of nearest peer REI agro (118 MT/hr).

Financials

Company took a positive step in converting long-term debt into WC loans since this amount is mostly utilized for stocking of grains(Basmati rice needs to be stored for a year atleast) and also the company is slowly deleveraging itself with D/E ratio going down from 1.4 in 2011 to 1.0 in 2014

-Tax rate already@30 % to remain stable

– Ratio of export sales to domestic is 1:1. Domestic market has shown higher growth in recent past

– Margin triggers going forward(sales mix, op . leverage ,economies of scale,cost efficiencies ). The company is expecting to raise capacity utilization levels at Dhuri plant from 40% to 65%

-Capital efficiency triggers going forward (reducing WC requirements etc). the company has shown huge improvement in working capital days from 389 in 2008 to 277 in 2013.

One big positive with KRBL, which also shows company’s brand strength is advances it receives from customers. (2013 figure : 176 cr)

– Company doesn’t require any major capex going forward 2-3 years as it already has enough capacity on board.

PEOPLE

-Buyback

The company took a wise decision of buying back its own shares owing to depressed prices of company’ stock and in twelve months leading to Feb 2014 , bought back 77,22,048 equity sharesat an average price of Rs 23.58 per share

-Promoter holding stands at 58.65% after buyback

– Promoter compensation(as a % of net Profits ) is 7.5%, which is on the higher side .

PRICE

As on 09 May 2014 , the company’s market cap is 1464 crs with Last year FY2013-14 profits of 255.11 crs ,quoting at a p/e of 5.7

If the company is able to increase profits moderately at 20-25% CAGR over next 3-4 years and with the help of a slight p/e expansion, we can have a good upside in this stock

RISKS

– Geo-political Risk

The middle east is the biggest importer for Indian Basmati rice and accounts for almost 35% of KRBL revenues. KRBL mostly exports to Saudi Arabia ,UAE, Iraq Kuwait . Any political turmoil in this region may adversely impact exports,

We had already seen in 2011-12 ,UN imposed sanction on Iran and it adversely affected company sales and profits showed a negative growth of ~30%.Since then, company is consciously trying to reduce exposure to Iran.

– Movement in foreign currency

– Fluctuations in raw material prices

– Regulatory changes

Why?

Q. They say they command a significant price premium over other brands, but why is it not leading to superior return on capital ?

The coming times should be better for the company as now many things seem to be falling in place.

-better financial structure

-branding

-better capacity utilization

-sales growth

-efficient mgmt. of Wcap

It should show improvement in ROIC in coming times.

Q. do they have inventory risk, since rice needs to be stored for a year atleast to distill its quality ? does food inflation over a longer term mitigate this risk ?

Q. which are leading consumption geographies,demand drivers ,demand growth patterns ?

– domestic demand

– export demand mainly from middle east

-EU(mainly UK), China are opening up as new markets for Basmati exporters

Q. The company had negative growth in profits and margin contraction in 2011-12. Why ?

2011-12 was a bad year for the company and basmati export industry as a whole.

UN imposed sanctions on Iran, Dollar payments couldn’t be made and later a rupee payment mechanism was established.

Q. Company follows the strategy of serving all price segments from rs 30/kg to rs 150/kg. Why all segments ?

Since penetration of organized sector is low in non –basmati segments and also seeing it as a scalable, company is serving lower-priced segments also. Although, non-basmati rice are a very small proportion of total sales of the company.

Q. Is it a structurally bad business by nature, since it has huge WC requirements (Basmati needs to be stored for a year).

Company has shown in recent past that better financial management and efficient capacity utilization can bring improvement in ROIC.

Q. Should it get auditing done by a more reputed firm, present auditors; Vinod Kumar bindal & co.

The note

Aurobindo Pharma is majorly a play on US generics space (patent cliff , huge potential market ). The company has a healthy mix of Formulations and APIs(57% formulations and 43-44% API).

The company has shown good R&D capabilities and mantained a good pipeline of drugs and approvals ..

The company had a bad financial year a year ago as it received sanctions on one of its unit (UNIT VI in February 2011by USFDA (losing around 35 million dollars of sales from that unit’s products ) and a huge forex loss(on restatement of fair value of liabilities and redeeming of Fccbs ).

The company is back on the recovery track with resuming of operations in the previously shutdown unit and better hedging policy, healthy cash flows .

A thing to be noted here is although the company is highly leveraged( outstanding long and short term loans of around 3400 crs with a D/E ratio of 1.3) .But with more than 90% of debt in foreign currency ,its net foreign receipts are adequate enough to cover the debt repayment over various maturity dates. Over the coming year , company has to pay back around 50 million dollars of loans, and management is confident enough of paying it out of internal accruals.

Business

The generic pharma industry in US is highly commoditized , many players , short product life cycles.

A company has to keep introducing new drugs to sustain as well as grow its revenue.

Introduction of generic form of a medicine usually involves high price erosion of 80-90% in comparison to the patented drugs price and there is more subsequent price erosion with more players getting the approval for same drug.

Moat

The company has a narrow moat in the form of R&D capabilities of complex molecules and cost arbitrage with India as a manufacturing base.

Other Indian pharma majors like Cipla ,Lupin, Sun , Dr reddys have a wider moat but not by a huge margin in the form of highly integrated structure of Sales & Distribution, Manufacturing and R&D capabilities .

Pricing power is very low in generic space but still companies try to find some niche pockets; like Aurobindo has shown higher margins in the injectables space .

The company envisions to have CRAMS as 15-20% of it sales in the longer horizon of 3-5 years . These contracts provide good revenue stability by being very long term in nature , but exact terms of these contracts are usually confidential.

With the current pipeline of drugs management seems confident of achieving 20% compounded growth in sales.

Financials

-margins over the years

Historically, the company has a EBIDTA margin of 17-18%; currently with Ebidta margins at around 15%; management expects a 200-300 basis points improvement over the coming 4-5 quarters

Ebitda margins are expected to improve with op. leverage accruing with capacity addition and better sales mix with increasing formulations and injectables .

The UNIT-Vi which was issued an import alert by USFDA had to be kept running for quality management , inspection checks etc and now with reinstatement of production , these costs will be absorbed and aid in a better EBITDA margin .

Management

The promoters have shown good managerial capabilities in scaling up the business across various geographies , and now company has hired experienced executives for its US operations as well.

Dangerous cocktail of promoter shares pledged and huge debt

As of March 2013, 23.46% of promoter shareholding is pledged (around 12% of total shares outstanding is pledged ) and the total debt is around 600 million dollars.

Valuation

Probabilistic scenarios

Good ( growth keeps momentum , more launches , margin expansion due to op. leverage and favorbale sales mix towards formulations and the cashflow improves reducing debt )

Base case( launches continue , forex fluctuations, ,no margin expansion due to significant inventory rampups , significant investments towards sales force and other things)

Bearish case (Delay in ANDA approvals hence ramping up sales will hurt the debt repayment schedule ,USFDA alerts to any other units.)

With sales growth , better margins and deleveraging of bal. sheet over coming 2-3 years ,there is a good potential upside from EPS growth and rerating.

Risks

Business slowdown

The biggest nightmare for any highly leveraged company is slowdown in business as it adds to interest costs and company may have to refinance loans on unfavorable terms.

Usfda

Dollar denominated debt

the company has to restate the fair value of liabilities every quarter and with rupee depreciating , it may prove to be a dampener for EPS .

US macro environment

satta king 786

hdhub4u

satta king 786

hdhub4u